US Equity Market Volatility Index

Download Data

We create a newspaper-based Equity Market Volatility (EMV) tracker that moves with the CBOE Volatility Index (VIX)and with the realized volatility of returns on the S&P 500. We also create a Policy-Related EMV Tracker and a suite of more than 30 category-specific EMV trackers that quantify the importance of each category in the level of U.S. stock market volatility and its movements over time. Our overall and category-specific EMV trackers are monthly and available from January 1985 to the present.

To construct our overall EMV tracker, we proceed as follows. First, we specify terms in three sets, as follows:

- E: {economic, economy, financial}

- M: {"stock market", equity, equities, "Standard and Poors" (and variants)}

- V: {volatility, volatile, uncertain, uncertainty, risk, risky}

Second, we we obtain monthly counts of newspaper articles that contain at least one term in each of E, M and V for eleven major U.S. newspapers: the Boston Globe, Chicago Tribune, Dallas Morning News, Houston Chronicle, Los Angeles Times, Miami Herald, New York Times, San Francisco Chronicle, USA Today, Wall Street Journal, and Washington Post. Third, we scale the raw EMV counts by the count of all articles in the same paper and month. Fourth, we standardize the scaled frequency counts for each paper to have a unit standard deviation from 1990 to 2015. Fifth, we average the standardized scaled counts over newspapers by month. In a final step, we multiplicatively rescale the resulting average series to match the mean value of the VIX from 1985 to 2015.

To construct our category-specific EMV trackers, we calculate the share of EMV articles in each category and multiply by the contemporaneous EMV tracker value. For example, to measure the importance of monetary policy considerations in equity market volatility during month t, we calculate:

where # denotes the count of newspaper articles in the indicated set, and EMV_t is the value of our overall EMV tracker in month t. We use this same approach for each category and a similar approach for our Policy-Related EMV tracker.

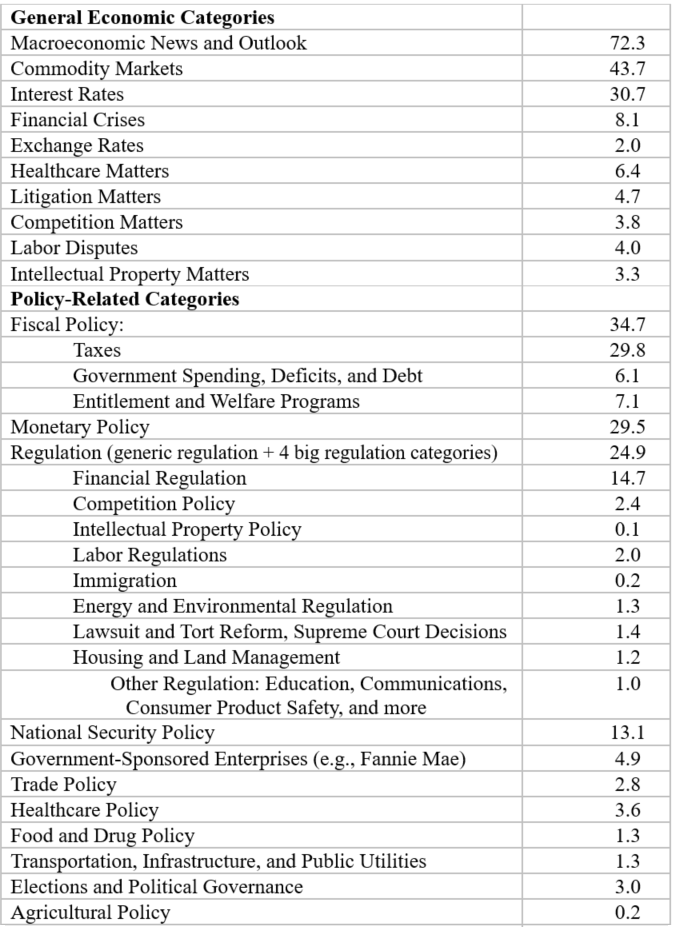

The following table lists our EMV tracker categories and the percent of EMV articles from 1985 to 2017 that contain one or more terms in each category:

For more information on our methods, term lists for each category, and a discussion of how we select terms, see "Policy News and Equity Market Volatility" by Scott R. Baker, Nick Bloom, Steven J. Davis and Kyle Kost.

We also construct an index that tracks "Infectious Disease Equity Market Volatility". Please see the linked page for data and further informatiion.

Our daily US Equity Market Uncertainty Index, which relies on different text sources and a somewhat different methodology, is available here.

This work is licensed under a Creative Commons Attribution 4.0 International License. © 2012-2018 by Economic Policy Uncertainty